ASML Q4/FY2024 Analysis

And my thoughts on the company's future

Last week, ASML published its Q4/FY2024 results. In this article, I dive into the most important figures and share my thoughts on the company’s performances. A disclaimer applies to this article. You can read this disclaimer at the bottom of this article.

ASML Q4-2024

Key Figures ASML Q4/FY2024:

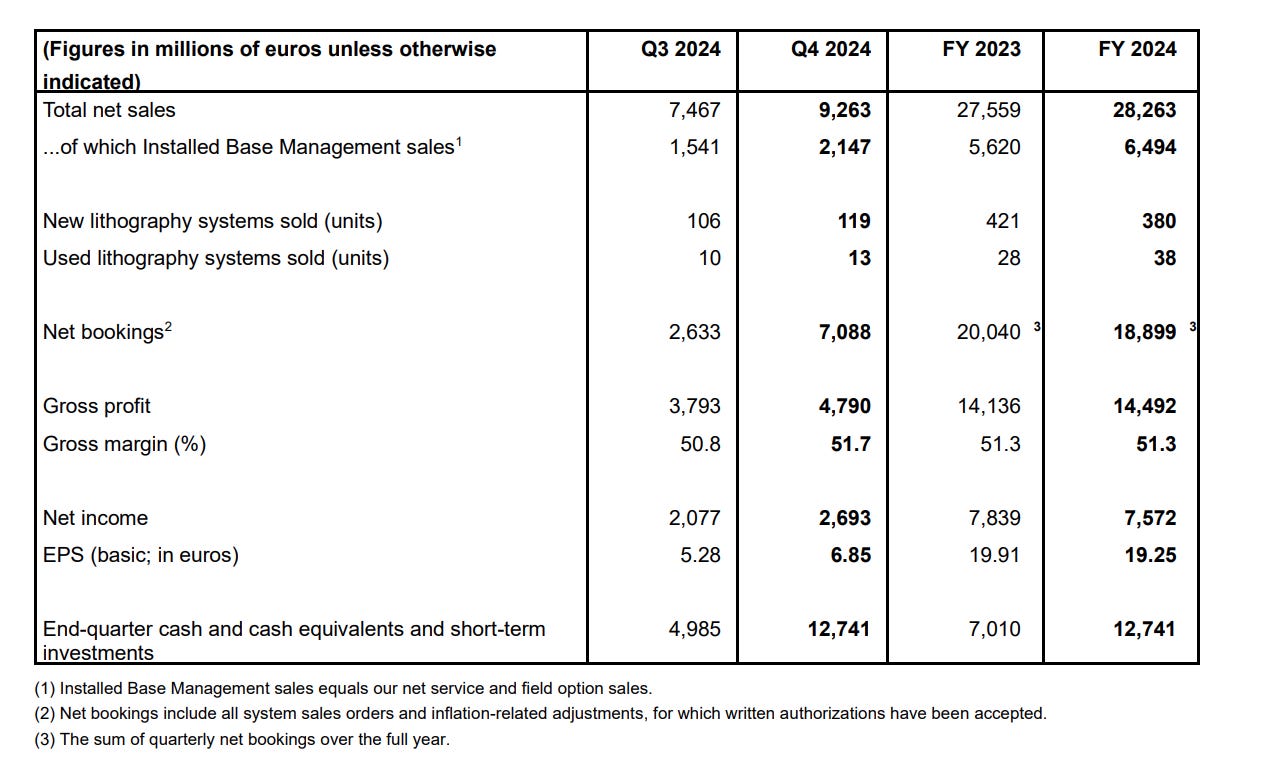

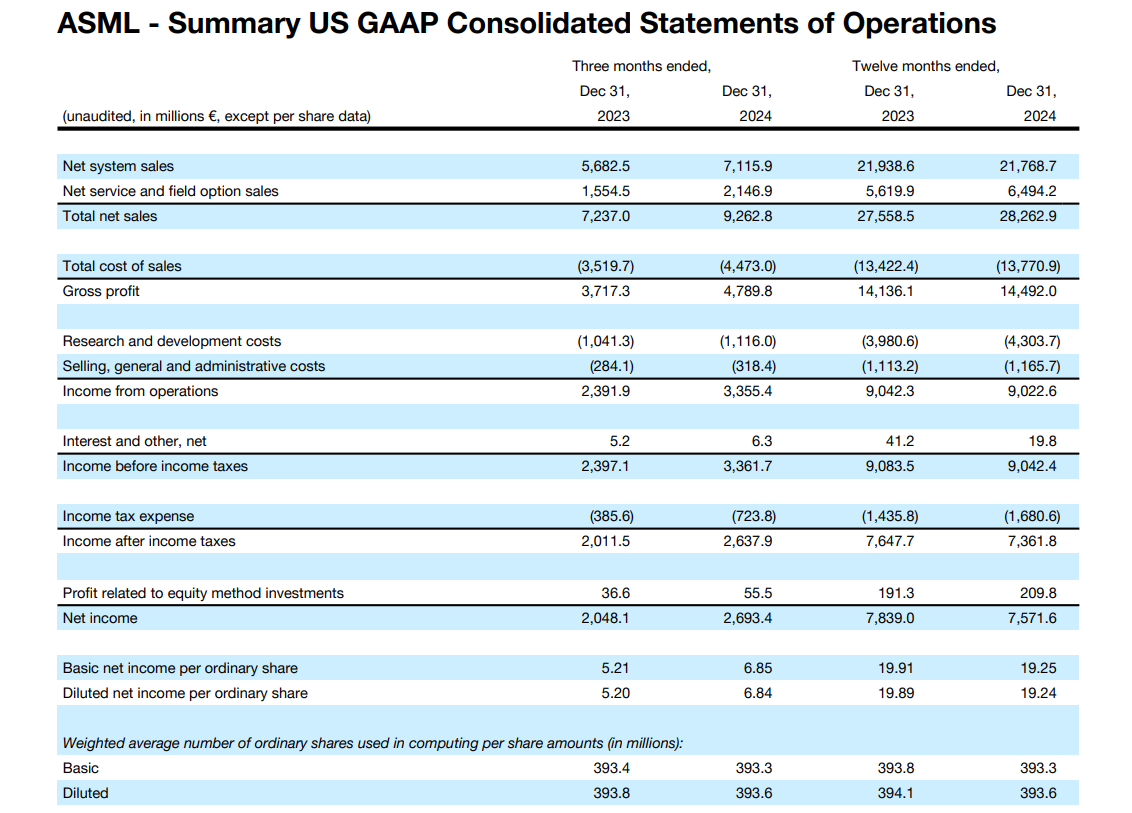

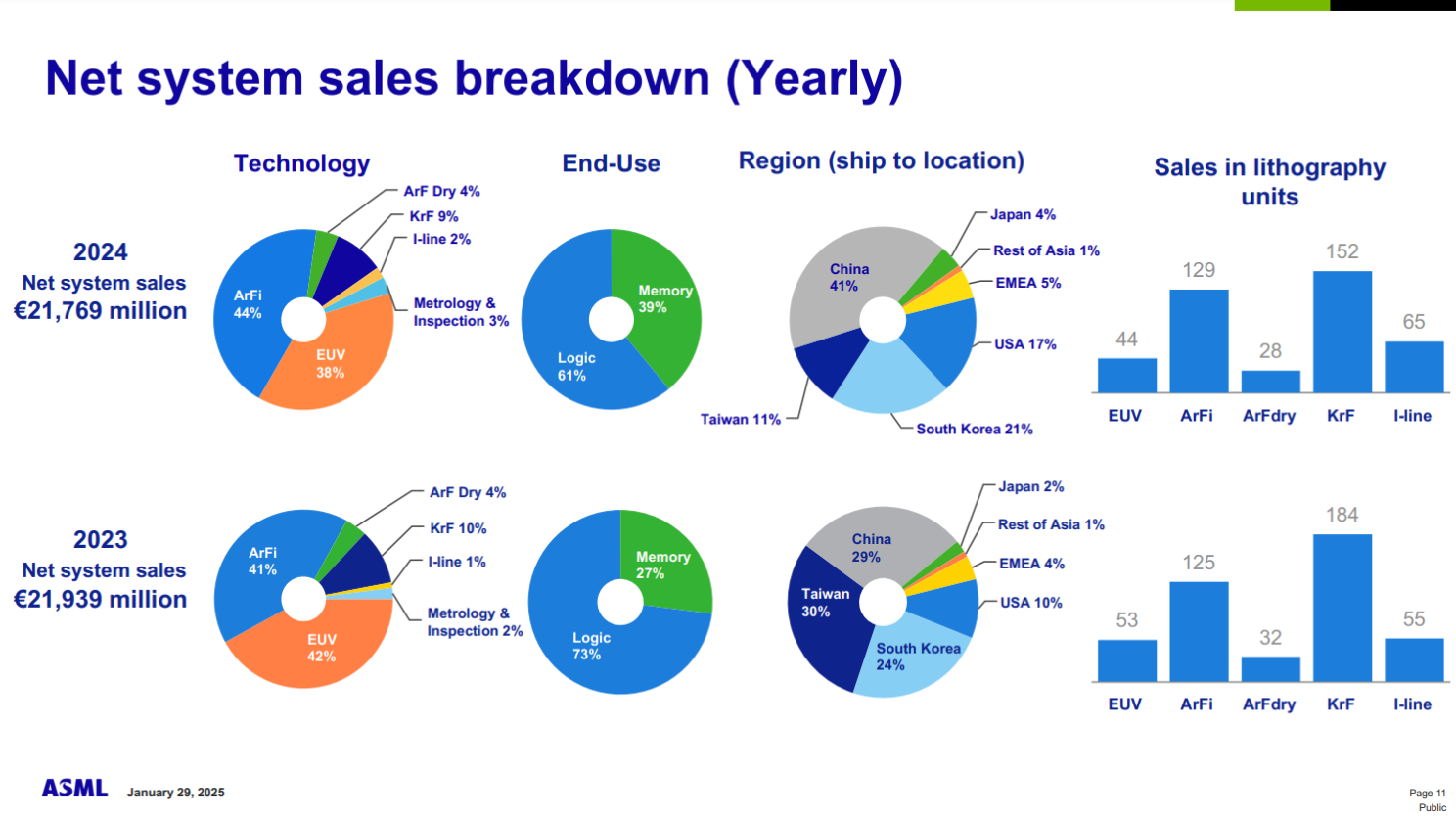

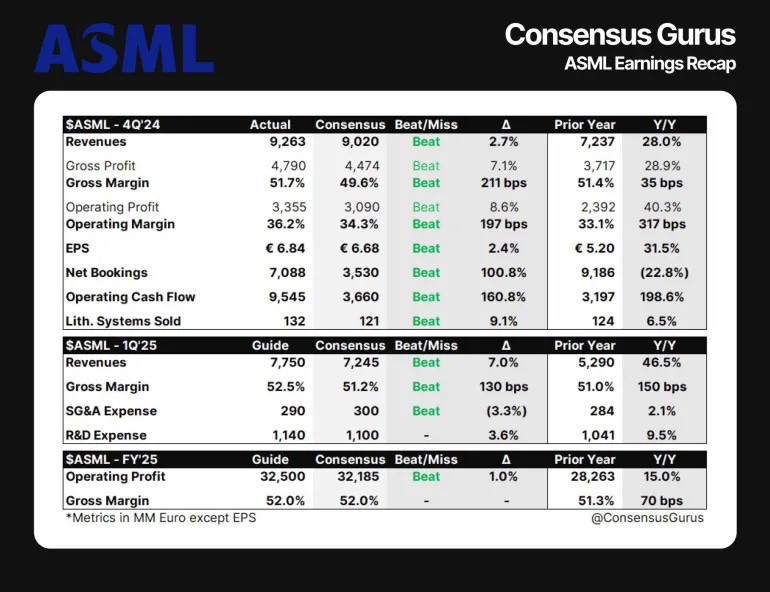

In Q4-2024, ASML reported total net sales of €9,263 million, broken down as follows:

€7,116 million in Total System Sales;

€2,147 million from Installed Base Management.

During its Investor Day on November 14, ASML projected revenue of €9 billion for Q4-2024. The company slightly exceeded this estimate, reaching €9.3 billion in revenue.

ASML recorded a gross profit of €4,790 million, resulting in a gross margin of 51.7%. Net profit for Q4-2024 amounted to €6.85 per share.

Our fourth-quarter was a record in terms of revenue, with total net sales coming in at €9.3 billion, and a gross margin of 51.7%, both above our guidance. This was primarily driven by additional upgrades. We also recognized revenue on two High NA EUV systems. We shipped a third High NA EUV system to a customer in the fourth quarter.

— Christophe Fouquet (CEO ASML)

In Q4-2024, ASML secured net bookings of €7,088 million, with €3 billion allocated to EUV systems. With net bookings roughly in line with total system sales, ASML's order backlog remained at €36 billion at the end of December 2024 (Q3-2024: €36 billion). This was confirmed by CFO Roger Dassen during the earnings commentary.

ASML FY-2024

ASML's total revenue for FY2024 amounted to €28,263 million, reflecting a 2.6% increase compared to FY2023.

For the year, ASML achieved a gross profit of €14,492 million (FY2023: €14,136 million), with a gross margin of 51.3%, unchanged from FY2023.

ASML achieved another record year, ending with total net sales for 2024 of €28.3 billion, and a gross margin of 51.3%.

— Christophe Fouquet (CEO ASML)

ASML reported a net profit of €7.572 billion for FY2024 (FY2023: €7.839 billion), translating to an EPS of €19.25 (FY2023: €19.91). Based on trailing twelve months (TTM) earnings, ASML is currently trading at a P/E ratio of 32.5. However, looking forward, this multiple is expected to be significantly lower—more on this later.

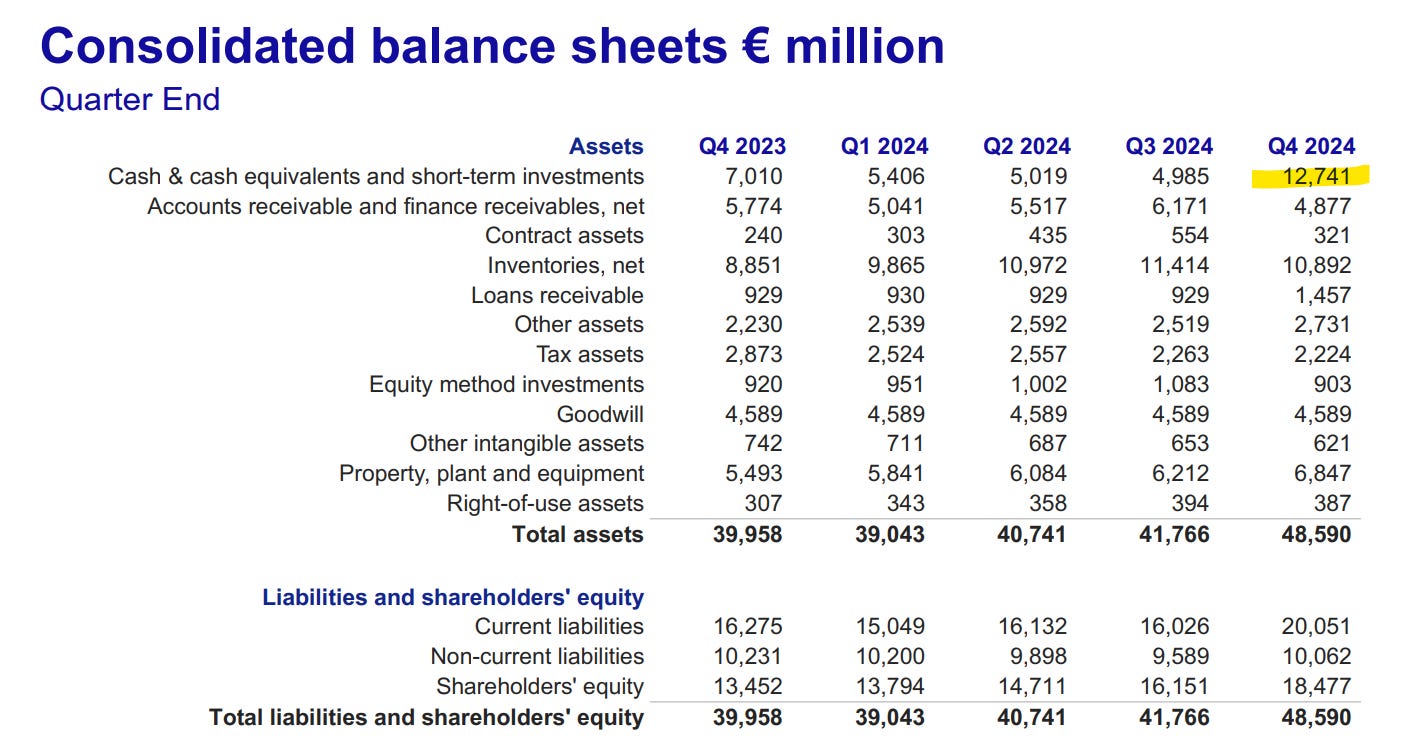

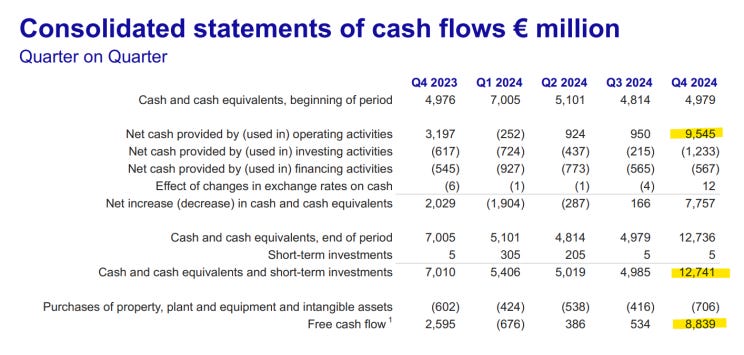

ASML is in a strong position, with cash & cash equivalents (C&CE) and short-term investments totaling €12.7 billion at the end of FY2024 (FY2023: €7 billion).

Net Bookings & Backlog

ASML's cumulative net bookings for FY2024 amounted to €18.9 billion, down from €20 billion in FY2023. Net bookings are a critical KPI as they provide insight into ASML’s future revenue.

In Q4-2024, ASML received €7.1 billion in new orders, a significant increase compared to €2.6 billion in Q3-2024. This fluctuation highlights the importance of evaluating ASML's order intake over multiple quarters, as order inflows are not a steady process.

Changes in Net Bookings Reporting

Starting in 2026, ASML will no longer report quarterly net bookings. Instead, it will disclose its order backlog once per year. This means that for three out of four quarters a key financial metric will be missing.

Historically, low order intake has negatively impacted media sentiment and stock price performance, as seen in Q3-2024 and past ASML quarters. A similar example occurred with Netflix in Q1-2022, when a temporary pause in subscriber growth significantly affected investor sentiment.

By stopping quarterly net bookings reporting, ASML is effectively removing a short-term market driver, forcing analysts and investors to adopt a longer-term perspective.

While I support encouraging long-term thinking, I believe transparency is even more important. This decision could therefore disadvantage long-term investors who rely on quarterly trends and TTM data.

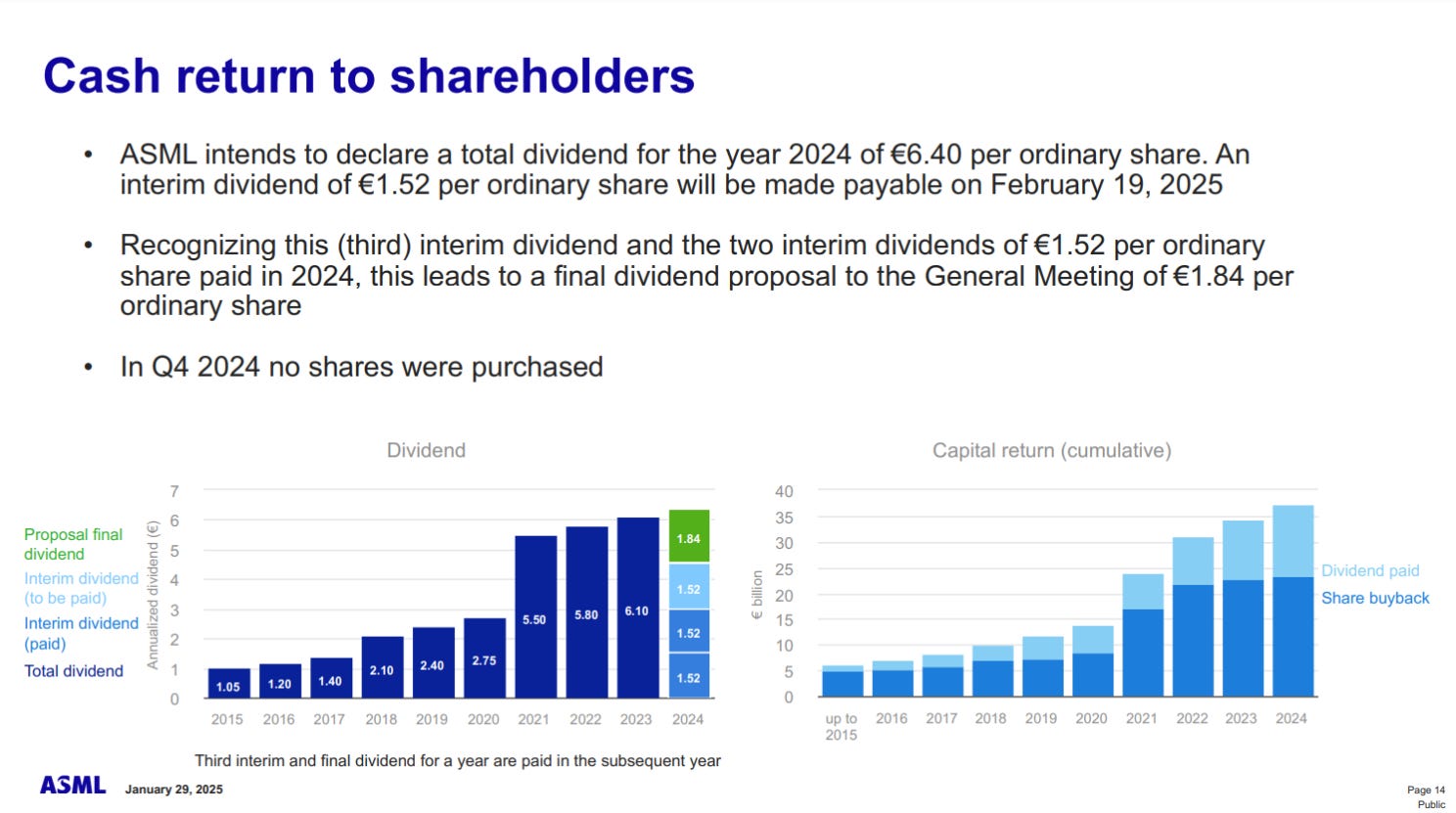

Dividend & Share Buybacks

ASML announced a dividend of €6.40 per share for FY2024, representing a 4.9% increase from FY2023.

Two interim dividends of €1.52 per share were already paid.

A third dividend payment of €1.52 per share is scheduled for February 19, 2025.

The final dividend payment for FY2024 will be €1.84 per share.

ASML did not execute any share buybacks in Q4-2024 under its 2022-2025 share repurchase program. Below an overview of ASML’s cash returns to shareholders since 2015.

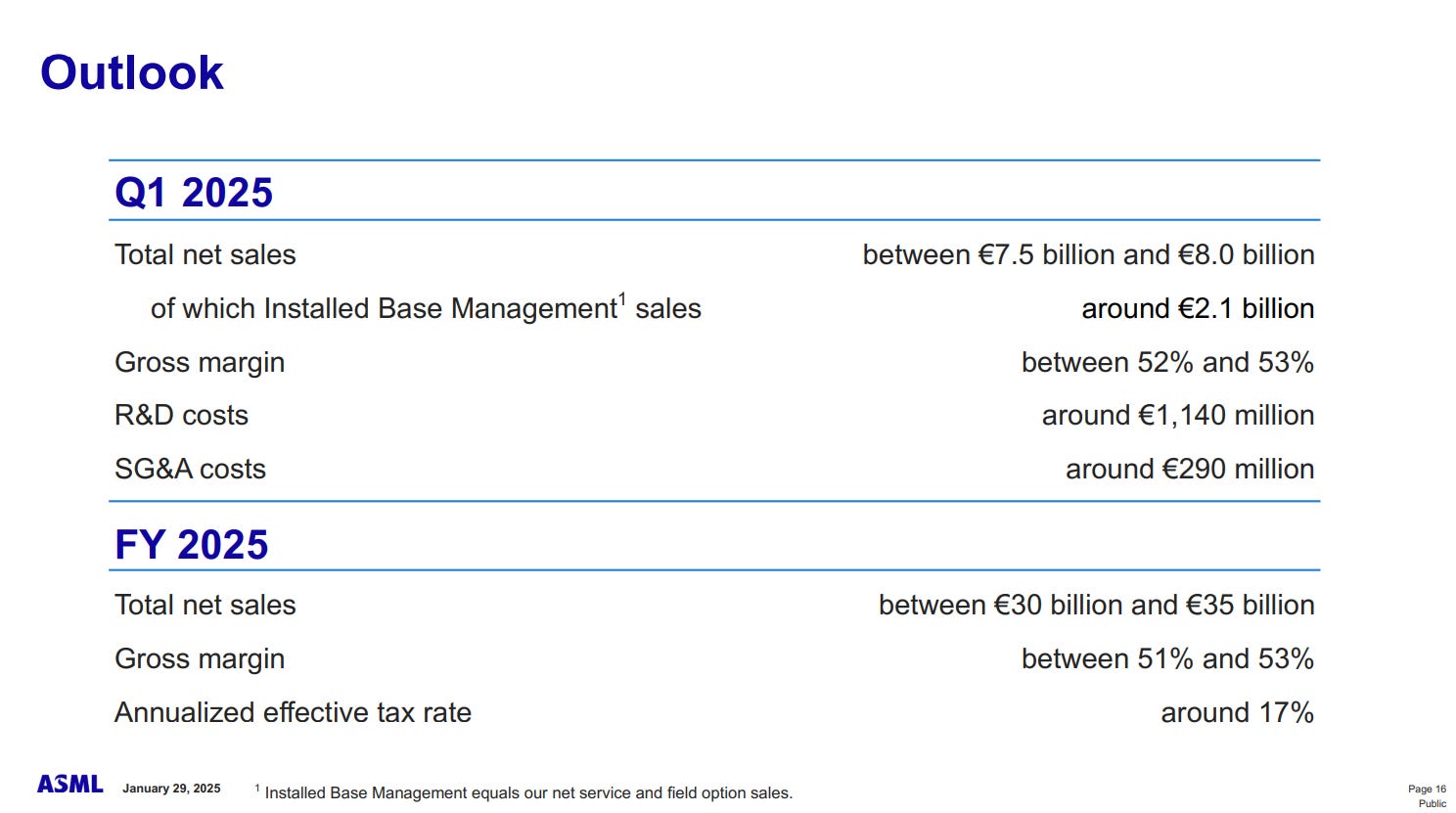

Outlook Q1/FY2025

For the first quarter of FY2025, ASML expects revenue between €7.5 billion and €8 billion, with a gross margin of 52% to 53%.

With an order backlog of €36 billion, ASML is already well-positioned for its FY2025 revenue, as the company expects total revenue of €30 billion to €35 billion for the year. ASML anticipates a gross margin of 51% to 53% for FY2025.

Consistent with our view from the last quarter, the growth in artificial intelligence is the key driver for growth in our industry. It has created a shift in the market dynamics that is not benefiting all of our customers equally, which creates both opportunities and risks as reflected in our 2025 revenue range.

— Christophe Fouquet (CEO ASML)

Press Conference

ASML’s press conference is avaible on its website. Below are the key points.

Christophe Fouquet: FY2024 was a transition year in many ways. AI played a central role and had a major impact on our industry. We are closing FY2024 on a very strong note and starting FY2025 on a solid footing.

Generative AI is expected to contribute $6 to $13 trillion to global GDP by 2030 (McKinsey, 2024). ASML is ready to support this growth. Christophe Fouquet emphasizes that ASML will drive advancements in both cutting-edge technology and mainstream products to support AI developments. AI will be a key growth driver starting this year.

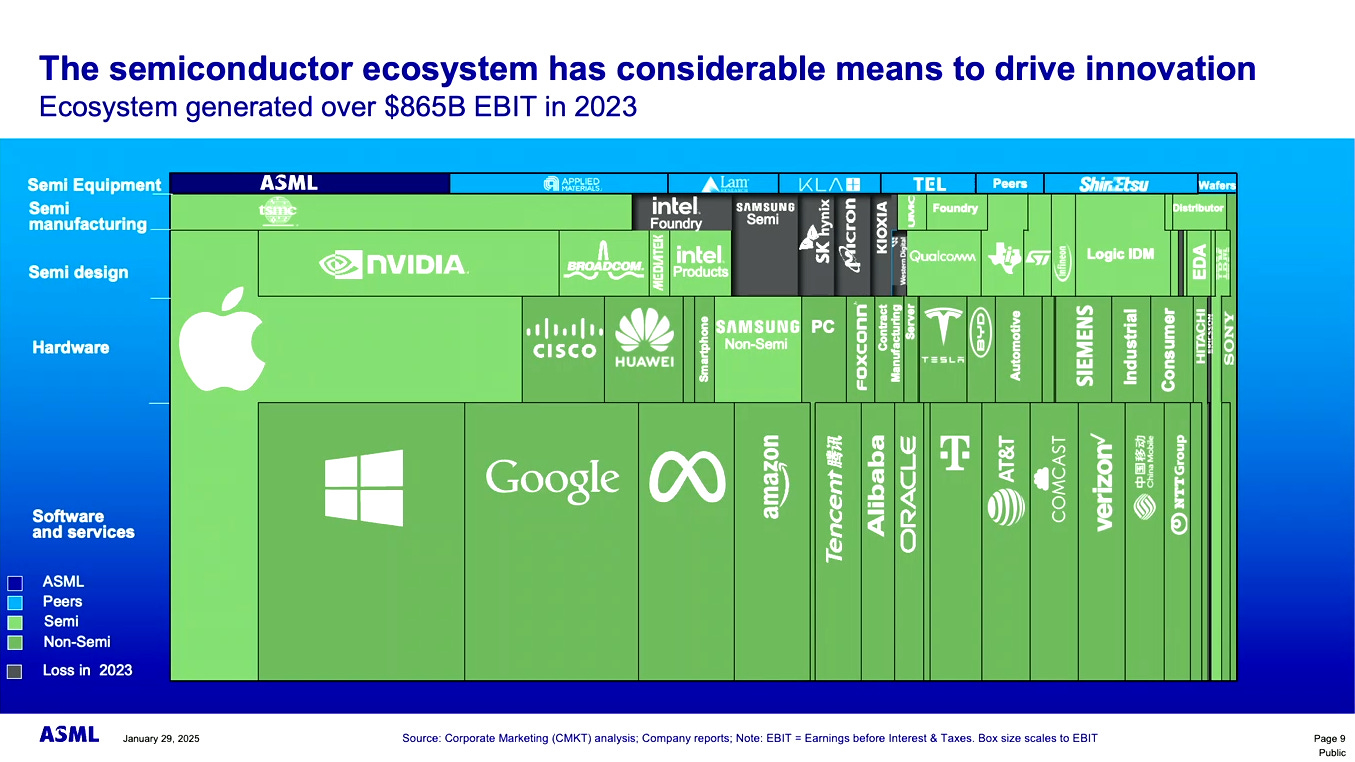

Below is an overview of the operational profits of end users and stakeholders in the semiconductor industry ecosystem.

Roger Dassen (CFO): Q4-2024 was a very strong quarter, with outperformance in several areas. We are closing FY2024 as a strong year.

ASML’s sales in China are expected to drop to the low 20% range of total revenue in FY2025, which aligns with China’s current share in ASML’s order backlog.

In FY2024, ASML continued to invest in R&D and will keep doing so, according to Roger Dassen.

Dassen noted that 90% of ASML’s cash inflow occurred in Q4, which he cites as the reason for its limited or even absent share buybacks in recent months. The only repurchase activity was 574,925 shares for employee share plans between January and April 2024.

Roger Dassen stated that the future looks promising for ASML and its technology roadmap. He reaffirmed ASML’s FY2030 targets of €44 billion to €60 billion in revenue with a gross margin of 56% to 60%.

Q&A

[Quotes are paraphrased and condensed]

The first question immediately addresses the "elephant in the room": DeepSeek. Christophe Fouquet responds:

We believe that AI expansion has 2 main challenges: 1) costs and power consumption, we need to see major progress of these two for us to see AI everywhere, and 2) Moore's law. Any technology that will contribute towards a cost reduction, is in fact good news for ASML. More applications means more chip demand. AI is a huge opportunity. Everyone wants to be in. Competition in software will be very high. Anything that will drive costs down will be a good thing for ASML in the long term.

— Christophe Fouquet (CEO ASML)

Was the DeepSeek market reaction on Monday overblown?

If you read the analyst reports, there is an increasing voice that in the end of the day, when you make it cheaper, it can lead towards a democratization of AI.

— Roger Dassen (CFO ASML)

Fouquet continues:

There will be a lot of new players; there will be a lot of competition. This will decrease costs, and will be in favor of innovation. [...] We look at the long term, because this is where the success, and opportunity, is. — Christophe Fouquet (CEO ASML)

According to Fouquet, there will be a shift in chip demand—from research on AI to the actual use of AI by consumers in various applications, including robotics.

Roger Dassen responds to a question regarding the decision to stop publishing net bookings on a quarterly basis:

At the end of the day, it matters to us that we give the right information. We think that the guidance that we provide, gives you better information than the QoQ numbers. Less is more. — Roger Dassen (CFO ASML)

Investor Call

The investor webcast is also available on ASML’s website. After reviewing the published figures, the Q&A session followed. Below is a summary of the key points.

Lower costs of installing High-EUV tools

Dassen: Costs were lower in the last quarter, and these expectations are reflected in the FY2025 figures.

Are Chinese orders declining faster due to potential upcoming regulations?

Dassen: The backlog in China has normalized, so revenue from China as a percentage of total revenue will also return to normal. Order intake in Q4-2024 was healthy and normal. ASML expects this normalized pattern to continue throughout FY2025.

Net Bookings

Dassen: Customers often place orders for multiple systems at once, usually within a single quarter. As a result, order intake can fluctuate between quarters. However, this does not reflect ASML’s underlying progress.

Therefore we expect that the market is better off [by not publicing Net Bookings anymore on a Q-basis].

— Roger Dassen (CFO ASML)

Strong demand for EUV due to AI. Will 2025 be a big build up year for 2026?

Fouquet: The ramp-up is definitely starting in 2025, followed by 2026 and 2027. He adds that ASML has so far observed a normal pattern in line with its stated expectations.

What are the plausible factors that could lead to revenue coming in at the lower end of the projected range?

Fouquet: Pushouts are possible, which is why we define a range. Geopolitical factors are more difficult to quantify.

Will 2026 be a growth year?

Dassen: We see 2026 as a potential growth year for ASML. However, it is too early to provide a definitive answer.

Forward-looking view on Logic?

Dassen: We expect to see order intakes for EUV in the first two quarters of 2025.

Conclusion

All things considered, the Q4-2024 results that ASML published last week are, in my opinion, good, with KPIs that all came in above analysts’ consensus expectations.

However, as I mentioned earlier in the article I wrote on January 26, Q numbers from ASML are not of paramount importance for long-term investors in the company. What matters are the long-term developments in the past—and their trend—as well as the outlook for the future.

By eliminating the reporting of ASML's net bookings starting in 2026, the management is putting even more trust in their hands, as the important KPI related to the order backlog will only be shared once per year. I disagree with Dassen's comment that ASML’s guidance provides better information than the hard numbers, as guidance is aimed at the future, while net bookings and order backlog data offer real figures from the past.

Revenue recognition can also fluctuate significantly from quarter to quarter, so I am concerned that the goal ASML has in mind may still be lost. We will see the market’s perception in 2026. For FY2025, the company will continue to report its order intake KPI, which could thus still bring some share price volatility.

Although, ASML could actually take advantage from this, alongside its long-term shareholders, by activating its share buyback program at these times. It is unfortunate to see that ASML has neglected this since September 2024, although you could also make positive points about ASML’s defensive (minimum) cash policy.

Valuation Analysis Update

Following the published figures, I have found no reasons to adjust my valuation analysis either positively or negatively.

For FY2030, I calculate with revenue of €52 billion and a gross margin of 58% (both in the middle of the guidance reiterated last week). To estimate net income, I am assuming the highest implied costs within ASML’s given range (i.e., R&D costs of €6.6 billion, SG&A costs of €1.9 billion, and an effective tax rate of 17%).

This results in an implied net income of just over €18 billion. With a slightly decreasing number of outstanding shares and continuing dividend payments, I arrive at an implied share price of €1,473 based on an EPS of €49 in FY2030, using a multiple of thirty times net income.

This includes an EPS CAGR of 16.9% through 2030 (for the period 2014-2024, this was a 21.5% CAGR).

At the current share price of €685, this scenario, including expected dividend payments, yields an IRR of 15.2%, which I believe provides sufficient room for lower performance than ASML’s moderate FY2030 scenario and/or for higher-than-expected (and possibly sustained) investment costs.

This case assumes that ASML can maintain its moat in the coming years. What management has indicated last week about the threats posed by DeepSeek to ASML confirms my views on the company: further efficiency gains can drive additional innovation, which is also expected to boost the use of AI products and services.

Also, read the article I wrote last week on Monday about the threats of DeepSeek to ASML, as well as a brainstorm where I share my expectations regarding AI and its deflationary effects on company moats (both in Dutch, if there is interest in an English version here on Substack, feel free to let me know).

Disclaimer: The information above is provided for general informational purposes only and should not be construed as investment, accounting and/or financial advice. You should consult directly with a professional if financial, accounting, tax or other expertise is required. On February 8, 2025, I held a long position in $ASML.